[Serenity Premium] Silicon Valley Bank Failure and How It Might Impact USDC

[Serenity Premium] Silicon Valley Bank Failure and How It Might Impact USDC

Or Might Not

In view of the closure of Silicon Valley Bank by FDIC, and the subsequent announcement of exposure by Circle, we have reviewed the annual report to provide some facts:

Announcements:

FDIC on Silicon Valle Bank: https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/silicon-valley.html

Circle on its exposure:

Analysis of Silicon Valley Bank (SVB) 2022 Annual Report (audited by KPMG)

Balance Sheet Overview

As stated in the annual report, SVB is financially solvent, with $222 billion assets, and $195 billion liability, giving an equity of $16 billion.

Source: https://ir.svb.com/financials/annual-reports-and-proxies/default.aspx

The Issue

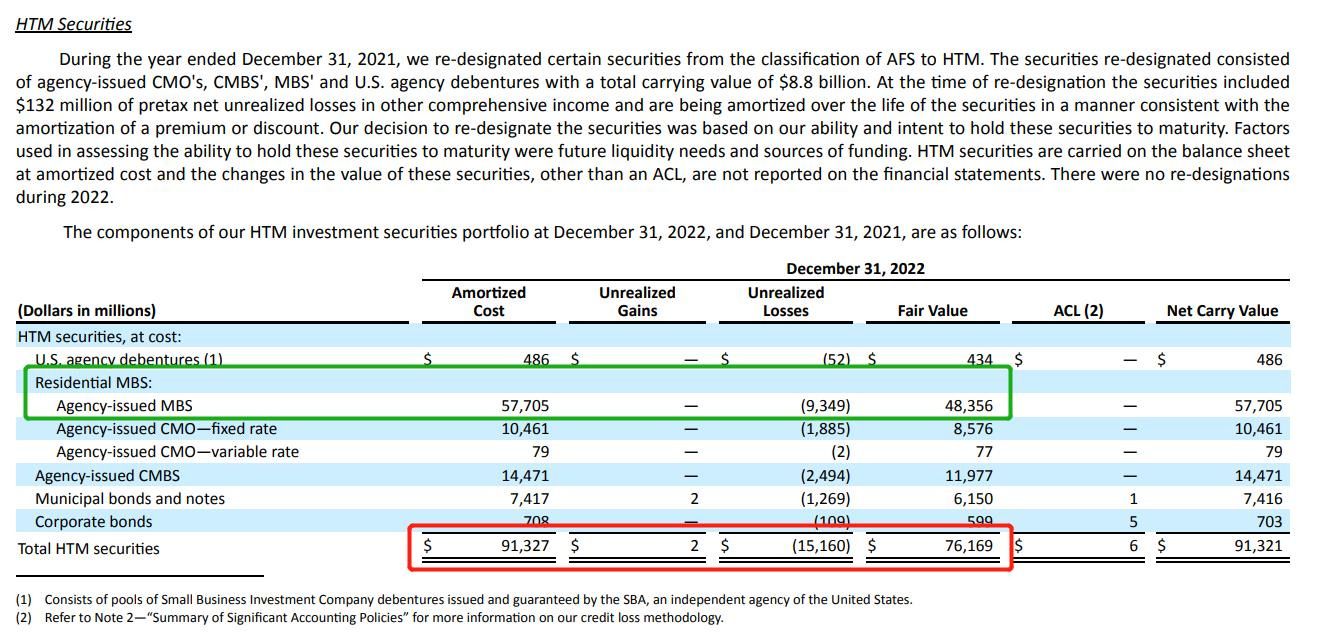

The issue with SVB is that some of its assets are not marked to market. In particular, its investments Held to Maturity (HTM). There’s no GAAP requirement to value all investments, especially those with long-term maturity to market value. Only short-term assets are required to mark-to-market.

As shown above, SVB had $91 billion of HTM assets recorded in its balance sheet, but its fair value is only $76 billion. If this asset is to be marked to market, the loss to SVB will be $15 billion. This will wipe out almost all of its equity.

For this reason or some other measurements by FDIC, SVB fails as an operating bank, and FDIC is intervening. Typically, FDIC will liquidate all assets and pay debts accordingly, over a period of time.

The Quality of Assets of SVB

There are four major classes of assets in SVB:

13.8 billion cash

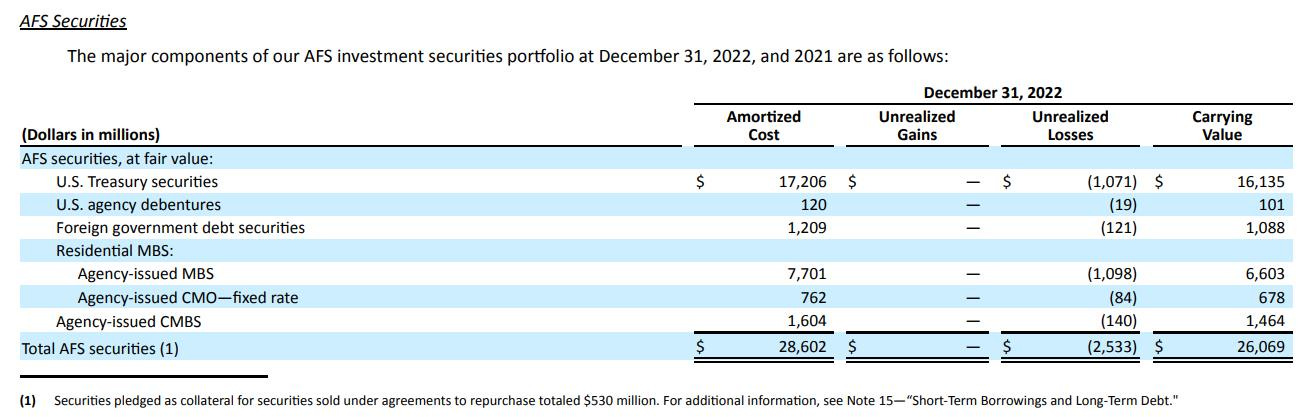

26.1 billion asset available for sales (AFS)

91.3 billion aforesaid HTM (fair value 76.2 billion)

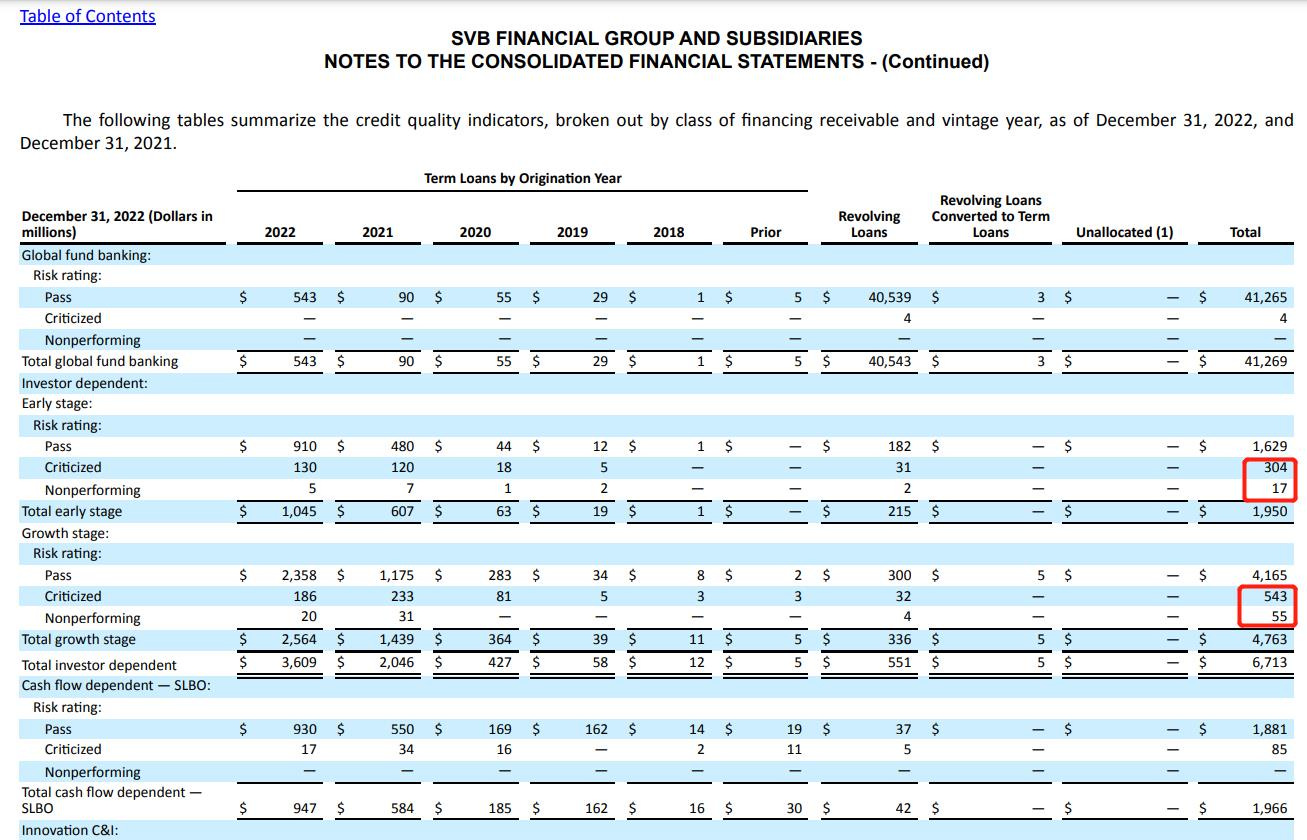

74.3 billion loan (less $2 billion in issue to make 72.3 billion)

The sum of the above after adjustment will be $188.4 billion, excluding other small classes of assets. This is 96% of all the $195.5 billion debt outstanding.

There’s no issue with cash. Both AFS and HTM are mostly US Treasuries, government debts and agency-issued mortgage bonds (e.g. Fannie Mae and Freddie Mac). AFS can be accounted as its book value, as it’s already marked-to-market (as of 31 Dec). HTM, after marked-to-market, are liquid assets by and large. So it might take FDIC some time to sell the HTM at its discounted fair market value, but they are not “gone”.

SVB’s loan book does not suggest anything significantly alarming. Out of $74.3 billion loans, there are about $2 billion that are in issue, mostly criticized only and not really non-performing.

Reason for SVB’s Trouble

There’s no details yet but judging from its financial statements, SVB bought Treasuries and MBS when interest rates were low and bond prices were high. As Fed has been hiking interest rate, fixed income assets have prices down. This translates into a book loss of $15 to SVB.

On the debtors side, it’s been reported that SVB’s clients, VCs and start-ups are cash-tight since 2022, as the Fed’ rates hike also made fund raising difficult. As a bank focusing much on VC and start-up companies, SVC sources more withdrawals than deposits over the period. Its investments also have longer maturities, making it hard to meet FDIC requirements.

Impact on Circle’s USDC

As stated above, purely based on the analysis of SVB’s 2022 Annual Report, FDIC should be able to liquidate SVB’s $188.4 billion assets (cash, AFS, discounted HTM, performing loans). This is 96% of all the $195.5 billion debt outstanding.

Circle is one of the debtors in the $195.5 billion and will get paid, in accordance to this ratio, after the due FDIC process, which might incur some fees and other senior classes being paid, e.g. taxes.

This is based on the assumptions: 1) KPMG had no material audit errors, e.g. undiscovered off-balance sheet items or other major senior debtors; 2) Assets prices did not worsen too much post 31 Dec, the time of marked to market; 3) Government bonds and agency-issued MBS have liquid market.

USDC, on the other hand, has $33 billion in US Treasuries as well, the interest of which (4.9% per annum on $33 billion, $1.6 billion) shall be able to cover the losses incurred here, if the FDIC could process a close to 96% repay of debts (4% of $3.3 billion, $0.1 billon).

However, the news have created much fear in the market causing a bank-run on USDC, with billons being redeemed. Investors also have concern that, in the event the bad debt in USDC is large than expected, e.g. somewhat $0.5 to $1 billion, a sizable bank-run could only allow the institutions to exit and even arbitrage. This will cause those with no direct redemption channels with Circle to suffer the residual loss. Market also has the fear that there’s more than SVB bank that has the issue.

{end of article}

Keep reading with a 7-day free trial

Subscribe to Serenity Research to keep reading this post and get 7 days of free access to the full post archives.